India Strategy : Nifty-500 review: Strong broad-based growth by Motilal Oswal Financial Services Ltd

Commodities lead; smallcaps shine

* Nifty-500 delivered strong double-digit earnings growth in 3QFY26, the highest in eight quarters, supported by improved sectoral breadth and benefits of GST 2.0 flowing through select sectors despite continued geopolitical headwinds.

* Aggregate earnings of the Nifty-500 Universe grew 19% YoY. Excl. Financials, reported aggregate earnings jumped 23% YoY. Excl. Metals and O&G, aggregate earnings grew 15% YoY.

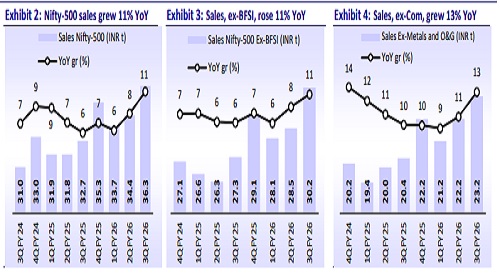

* Notably, aggregate sales for the Nifty-500 Universe grew 11%, the highest in 11 quarters, indicating a pickup in momentum. Aggregate sales/EBITDA/adj. PAT of Nifty-500 companies grew 11%/12%/19% YoY to ~INR36t/INR8t/INR4t in 3QFY26

* Commodities at the front: 3Q corporate earnings were driven by broad-based growth, with significant contributions from commodities – O&G (38% YoY) and Metals (34% YoY) – and robust contributions from key sectors such as PSBs (18% YoY), NBFC-Lending (19% YoY), Auto ex-TMPV (27% YoY), Capital Goods (24% YoY), Consumer (13% YoY), Telecom (160% YoY) and Retail (34% YoY). Moreover, Infra (28% YoY), Retail (34% YoY), NBFC Non-lending (29% YoY), Cement (46% YoY), Consumer Durable (36% YoY), EMS (36% YoY) posted healthy gains. In contrast, Pvt. Banks (3% YoY) and Chemicals (2% YoY) posted muted growth, whereas Utilities (-5% YoY) dragged down the overall performance.

* Largecaps’ momentum picks up; smallcaps outperform: The 3QFY26 earnings performance of the Nifty-500 was fueled by mid- and small-cap companies. Aggregate earnings of the Nifty Midcap-150 companies grew 20% YoY, while Smallcap-250 companies recorded 26% YoY growth on soft base. In comparison, the aggregate earnings growth for the Nifty-100 constituents stood at 18% YoY

* Sectors and companies: Of the 22 key sectors, 18 reported double-digit profit growth in 3Q. O&G and Metals dominated, collectively accounting for ~38% of the incremental YoY accretion in earnings. About ~50% of companies (245) in the Nifty-500 reported earnings growth of over 15% YoY, while 27% of companies (134) reported a decline or loss in 3Q. The top 10 incremental profit contributors, primarily from O&G, Metals, Financials, and Telecom, together contributed around 50% of the incremental YoY earnings growth.

* EBITDA margin of the Nifty-500 (excl. BFSI) came in at 16.8% (up 30bp YoY, down 60bp QoQ) in 3QFY26. Excl. commodities (Metals and O&G), EBITDA margin stood at 19.1% (down 80bp YoY/90bp QoQ). Six out of 17 major sectors (excl. Financials) reported EBITDA margin expansion during the quarter.

* 9MFY26 performance: Earnings of the Nifty-500 universe grew 15% YoY in 9MFY26. Excl. Financials, the earnings grew 19% YoY, while excl. Metals and O&G, the earnings rose 12% YoY. The large-/mid-/small-cap earnings increased 13%/23%/21% in 9MFY26.

Key sectoral highlights for 3QFY26

* Oil & Gas: The sector contributed significantly to the aggregate earnings growth during the quarter, with EBITDA/PAT growth of 27%/38% YoY, mainly led by OMCs. Excl. OMCs, the O&G sector’s EBITDA/PAT grew 8%/7% YoY in 3QFY26.

* Metals: The sector reported strong PAT growth of 34% YoY over a soft base of 3% growth in 3QFY25. Growth was also boosted by a flat performance of ferrous companies, supported by volume recovery but offset by softer realization. EBITDA grew 4% YoY over muted NSR. Non-ferrous companies posted strong earnings growth, led by favorable metal prices and steady volumes.

* BFSI reported 13% YoY earnings growth, primarily led by PSBs (18% YoY) and NBFCs (19% YoY), while Private Banks posted a muted 3Q performance (3% YoY). The banking sector posted a steady quarter, supported by stable margins, healthy loan growth and continued improvement in asset quality, with credit costs remaining well under control. We project sector credit growth to remain at ~12.5% YoY for FY26. NBFC-Lending companies delivered a mixed performance in loan growth, with signs of demand revival visible in vehicle finance (post-GST rate cut).

* Automobile segment saw a healthy revival in demand momentum in 3Q, with all segments recording double-digit volume growth after a muted 1H, aided by the festive season and the benefit of the GST rate cut. Aggregate sales/EBITDA/PAT (ex-TMPV) grew 19%/18%/27% YoY in 3QFY26.

* Cement sector reported its third quarter of strong earnings growth, rising 46% YoY after four consecutive quarters of earnings decline. Reported sales and EBITDA of the sector grew 19% and 17% YoY, respectively, backed by healthy demand recovery of ~7-8% YoY during the quarter.

* Telecom sector reported a profit of INR31b in 3QFY26 compared to a profit of INR12b in 3QFY25, primarily driven by Bharti Airtel. However, other peers posted healthy growth or a decline in earnings for the quarter.

* Capital goods companies reported a healthy quarter, with sales/EBITDA/PAT growth of 11%/6%/24% YoY, supported by healthy order inflows and execution. Overall, government-led spending in power T&D, defense and renewables, along with selective private capex in real estate, digital infrastructure and data centers, continues to support a constructive ordering outlook.

* Consumer sector reported its first double-digit earnings growth in seven quarters, with a 13% YoY increase. Staple companies saw resilient demand and remain optimistic about a steady consumption recovery in the coming quarters. Key government initiatives, along with milder inflation, improved affordability following recent GST rate rationalization, and declining interest rates, are supporting both rural and urban consumption.

* Technology: IT companies posted positive earnings growth, the highest in 10 quarters, despite seasonally weak conditions in 3QFY26. They reported betterthan-feared earnings, with PAT growth of 12% YoY. Management commentary on discretionary spending and early AI-related demand remained constructive, though broader sentiment turned cautious after AI-native players like Palantir and Anthropic highlighted faster AI-led productivity gains, compressed implementation timelines, and potential disruption across applications, fueling debate on AI-driven deflation versus incremental revenue opportunities.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412