OmniScience Capital expects Nifty 50 to reach between 28,000 - 31,000 level during FY27

OmniScience Capital estimates the FY27 Nifty 50 EPS (earnings per share) to be around INR 1280 to INR 1320. With P/E multiples ranging from 22 to 24, the Nifty 50 is expected to be in the 28000 - 31000 range by the end of March 2027, implying a 15% to 25% upside from the current levels.

Nifty’s upward trajectory is fundamentally supported by earnings expansion, with growth estimated at 10%–13% for FY27. OmniScience Capital also expects a potential re-rating driven by easing geopolitical tensions, moderating crude prices, a strengthening INR, and a softer inflation outlook. These factors could enable the RBI to hold interest rates steady and also support renewed FII inflows. In the last 25 years, Nifty 50 has delivered ~14.26% CAGR incl. dividends exhibiting a sustained long-term uptrend, punctuated by sharp but relatively short-lived drawdowns, reflecting the underlying growth in earnings and liquidity support over time.

Vikas V Gupta, CEO & Chief Investment Strategist, OmniScience Capital said, “Market is significantly undervalued and even at moderate earnings growth rate returns are likely to be quite rewarding for the long-term investors who can tolerate volatility.”

Banking – Strong System & Capex Tailwinds

Banks are in their best shape in a decade with GNPA below 2.5%, CRAR around 17%, and PCR near 76.6%, indicating robust balance sheets. This positions them to fund incremental credit of ~?94 lakh crore without fresh equity. A sustained government and corporate capex cycle should drive multi-year credit growth and earnings visibility.

Power – Energy Transition & Capex Supercycle

India’s power sector is entering a structural S-curve, with renewables, storage, and green hydrogen driving a shift toward ~74% installed capacity by 2035. A ?65–70 trillion capex opportunity, backed by strong policy support, underpins long-term growth. Rising electricity demand—potentially tripling—along with new-age consumption (EVs, data centers) adds durable visibility.

IT – Valuation Caution Amid Uncertainty

Despite recent corrections, IT stocks remain at fair-to-elevated valuations relative to growth visibility. Ongoing uncertainty around AI disruption and global tech spending warrants caution. It may be prudent to wait for clearer demand trends and more attractive entry points before increasing exposure. While the valuation from the long-term view point looks attractive, the issue is with the near to medium term growth outlook.

Ashwini Shami, President & Chief Portfolio Manager, OmniScience Capital said, “We are overweight on banks, financial services, and the power sector, driven by strong earnings growth, healthy balance sheets, and significant capital allocation toward capacity expansion. While we have traditionally been bullish on IT, the impact of AI on Indian IT remains uncertain, resulting in limited growth visibility over the medium term (2–3 years).”

Market Valuations Close to Long-term Averages: P/E ~21, P/B ~3.3

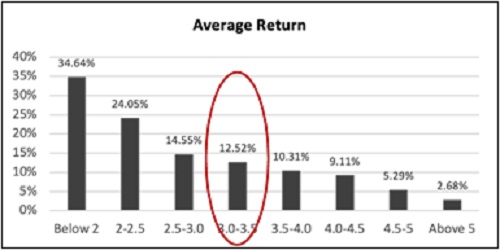

According to the latest report titled, “FY2027 Outlook: Resilient Economy Drives Return Potential In Undervalued Market” released by OmniScience Capital, markets could potentially deliver returns higher than the long term average return based on the historical analysis of index returns grouped by P/B buckets.

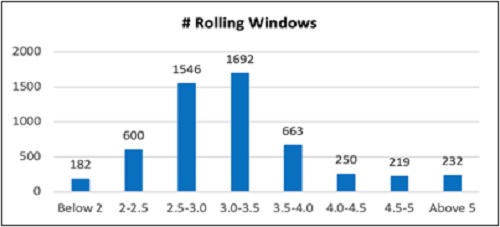

From a valuation standpoint, P/E and P/B multiples indicate that the market is currently at or below long-term averages but below prior cycle peaks. Current P/E is at ~20x and P/B is at ~3x.

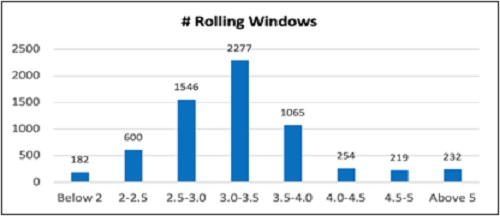

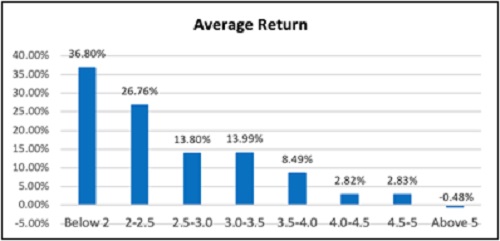

1-year returns show a clear inverse relationship with starting valuations, lower P/B regimes (<2, 2–2.5) deliver materially higher returns, while outcomes compress sharply as valuations rise, turning decisively negative beyond 5x P/B.

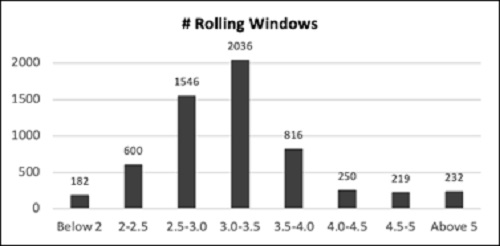

3-year returns continue to exhibit a strong dependence on starting valuations, though the gradient is less steep than in 1-year returns. Returns compress meaningfully as valuations rise but it suggests that valuation impact moderates over longer holding periods but does not disappear.

5-year returns show a clear but more gradual relationship. Unlike shorter horizons, even higher valuation buckets (>4) generate positive returns, indicating that time helps mitigate valuation risk. The decline in returns from low to high valuations is smoother, suggesting that earnings growth and compounding play a larger role over longer periods, reducing the impact of entry multiples.

Above views are of the author and not of the website kindly read disclaimer