The Corner Office Interaction with the CEO Mr. Ashok Vaswani, MD & CEO, Kotak Mahindra Bank by Motilal Oswal Financial Services Ltd

Growth anchored on responsible, safe banking Credit cost set to normalize; growth trends getting broad-based

We met the top management team of Kotak Mahindra Bank (KMB), represented by Mr. Ashok Vaswani (MD & CEO), Mr. Devang Gheewalla (Group CFO), and Mr. Kaynaan Shums (Head IR & Sr. EVP), to discuss the bank’s growth strategy, progress on liability franchise, profitability outlook, and other key focus areas. Following are the key takeaways from the discussion:

Growth remains healthy; focus remains on quality over volume

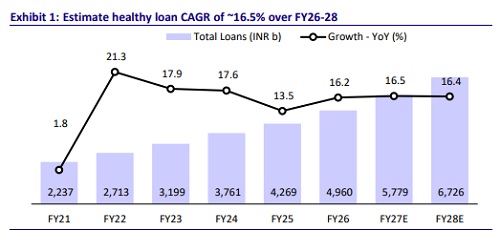

KMB continues to pursue a calibrated growth strategy, with the bank reiterating its objective of growing advances at 1.5-2.0x nominal GDP growth while maintaining prudent risk standards. Average net advances grew 16.2% YoY in FY26, supported by strong momentum in SME and mortgage businesses, both of which delivered growth of over 18% YoY. The bank has identified four strategic customer segments: Private Banking & Solitaire, Core India, SMEs, and Corporate/Institutional Banking, and is building differentiated propositions around each segment. The SME franchise remains a key growth driver, with growth healthy at 19% in FY26. Unsecured retail growth has started improving sequentially, with disbursements gradually recovering, while the unsecured mix remains stable at ~9% of advances. Management remains focused on profitable and sustainable growth rather than maximizing balancesheet expansion, believing that excessive growth could dilute returns and impact underwriting standards. We estimate loan growth at 16.4% CAGR over FY26-28.

Liability franchise remains a key strategic focus

Strengthening the liability franchise remains one of the bank’s key strategic priorities. Deposits grew 15% YoY in FY26, broadly in line with loan growth, while average deposits increased 14.9% YoY. The bank continues to focus on building multiple liability engines through affluent banking, SME relationships, corporate transaction banking, and the Kotak 811 platform. Current account balances grew 23% YoY, while fixed-rate savings balances increased 18% YoY, helping CASA improve to 43.3%. The Kotak 811 franchise continues to scale well, adding ~250-300k customers every month, with 811 savings balances growing 32% YoY and now contributing ~12% of the total savings book. Management remains confident that digital acquisition can continue to drive granular liability growth, while branch expansion from ~2,276 currently to ~3,500 branches over the next three to five years will further strengthen franchise penetration

CASA growth and asset mix improvement (including unsecured loan recovery) to keep margins steady

Despite a cumulative 125bp repo rate reduction during FY25-26, KMB delivered resilient margin performance. Reported NIM continues to stay healthy at 4.67% in 4QFY26 versus 4.54% in 3QFY26; adjusting for quarter-day count impact, management indicated that margins were broadly stable sequentially. The impact of lower lending yields was offset by deposit repricing and continued growth in granular low-cost deposits. NIMs can remain under check over the near term, led by the recent increase in TD rates and rationalization of day-count impact. However, recovery in retail loan growth, including unsecured assets, driven by normalization in the MFI segment, along with a revamped credit card business and healthy CASA growth, is expected to keep costs under control. With the introduction of the new FCNR scheme, the bank is actively looking to raise resources through this avenue. Its strong CASA franchise and relatively low cost of funds provide the flexibility to navigate a lower rate environment.

Asset quality outlook healthy; credit cost to normalize

The asset quality trend has improved over recent quarters, with gross NPA declining to 1.20% and net NPA reducing to 0.25% as of Mar’26. Slippages declined sharply to INR10.2b in 4QFY26 from INR16.1b in the previous quarter, while credit cost moderated to 39bp from 63bp in 3QFY26. Management highlighted that improvement was driven by better collections across granular retail portfolios, particularly commercial vehicles, microfinance, and credit cards. Importantly, there were no significant corporate recoveries or one-off resolutions during the quarter, indicating that the improvement was operational in nature. The secured portfolio continues to exhibit negligible stress, and management noted that it has not yet observed any signs of macro-led asset-quality deterioration despite global uncertainties and the West Asia crisis.

Capital position remains among the strongest in the sector

KMB continues to maintain one of the strongest capital positions among large private banks. As of Mar’26, standalone CET-1 stood at 21.3%, while capital adequacy remained robust at 22.4%. Management continues to classify capital into operating capital, financial infrastructure investments, and surplus capital. Excess capital is being deployed selectively into alternate asset opportunities and financial market infrastructure investments, while inorganic opportunities continue to be evaluated through the lens of strategic fit, valuation discipline, and management bandwidth. The strong capital position provides significant flexibility to support future growth while preserving balance sheet resilience.

Valuation and view: Reiterate BUY with a TP of INR470

* KMB has delivered healthy growth across advances and deposits while maintaining strong asset-quality metrics and one of the highest capital buffers in the sector.

* The bank’s strategic focus on affluent banking, SME lending, and digital customer acquisition provides a long runway for sustainable growth, though execution on liability mobilization and cross-sell remains critical.

* Improving credit costs, stable asset quality, and continued operating leverage should support earnings growth over the medium term.

* Management continues to target a business model capable of generating high-teen RoE over time, aided by contributions from subsidiaries, while maintaining prudent risk standards and strong capital buffers.

* We currently estimate KMB to deliver RoA/RoE of 1.96%/12.1% in FY27. Reiterate BUY with a TP of INR470 (2.1x Sep’27E ABV + INR165 for subs).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

MOSt Market Roundup : Nifty Opens 300 Pts Higher at 22695 on Positive Global Cues by Motilal...